U.S. Yield Curve – Studying the historic cycle

Yield curve is a graphical representation of interest rates at varying maturities. Short term interest rates are influenced by Central Banks/U.S. Federal Reserve Policy. These short- term interest rates rise when the Federal Reserve is expected to raise the rates and falls when it’s expected to cut interest rates. The rest of the yield curve is determined by an open market so to speak. Long-term bonds are influenced by factors such as demand – supply, inflation outlook and economic growth.

Types of Yield Curves

In 2017, as we see in the graph on the left, this type of yield curve is called “Normal Yield Curve”. This is the most common yield curve also known as “positively sloping yield curve” where the yields are lower for shorter maturity bonds and increase steadily as we move towards higher maturities. Such a yield curve also implies stable economic conditions.

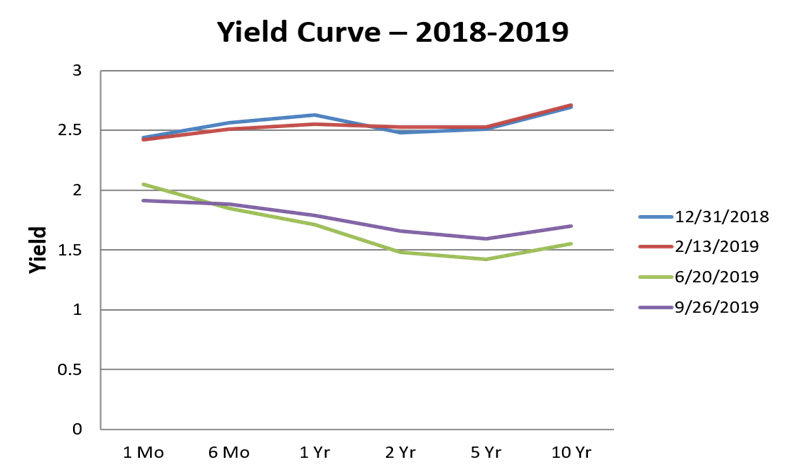

From 2016 to 2018, The FED continued to increase the shorter-term interest rate target (a target of 2.25% to 2.5% in December of 2018) due to continued strengthening of labor markets and economic activities. A strong economy also depicts that consumers and businesses are financially stable to access credits at higher interest rates. In 2018, the Fed Reserve was also shrinking/unwinding their balance sheet by letting the bonds mature or run-off without replacing them.

Albeit we saw the flattening of the yield curve in later half of 2018. This occurs usually when the yield on long term securities falls or short-term rises more than the longer term that leads to flattening of the curve, also flatten occurs when there is a transition between the normal yield curve and inverted yield curve. Long-term debt instruments are riskier than short-term, and they fluctuate more.

In 2019, the Federal Reserve cut interest rate for the first time since the recession (2008) due to impact of trade war and global slowdown of economies. The move taken by the FED was considered as favorable and just as “an insurance against potential speed bumps for the economy, including rising trade tensions and slow down in global economic growth”. However, the yield curve now slightly titled toward downwards.

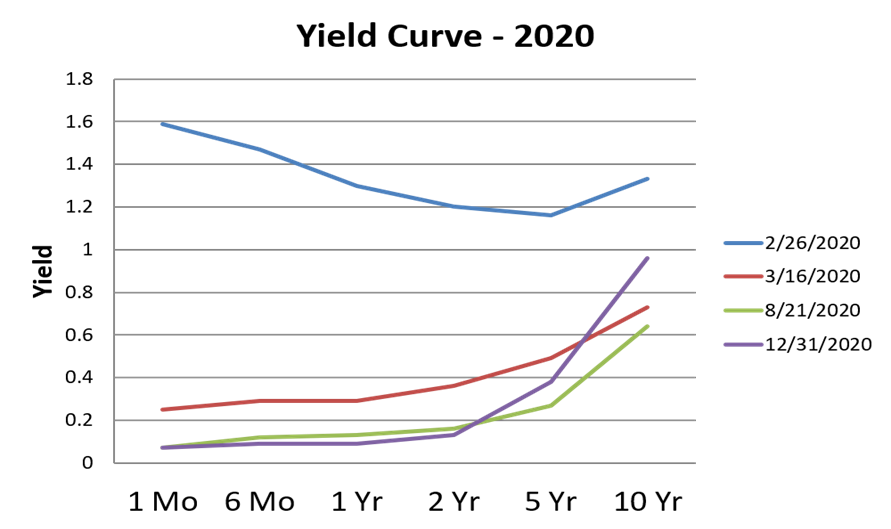

As we can see in the graph, in February 2020 the yield curve titled towards inversion (investors were growing concerned about COVID-19 pandemic).

The “dreaded inverted curve” occurs when the yields on short-term Treasuries are higher than yields on long-term Treasuries. A prolonging inverted yield curve is also considered a sign of recession or bear markets. Bond investors are sensitive to the Fed’s actions and comments regarding future interest rate outlook and economy. As investors flock to the long-term Treasury bonds, the yields fall, and bond prices go up (see-saw effect). The demand for long-term bonds increases as investors believe that they will make more by holding longer maturities in the event if recession is onset.

In March of 2020, due to the coronavirus outbreak, the FED took an emergency move of dropping the short-term rates to near zero and launched several quantitative easing programs. As we see in the chart, the yield curve is now steeping. The gap between short- term bonds and long-term bonds increases. Again, the shorter end of yield curve is influenced by Central Banks policies.

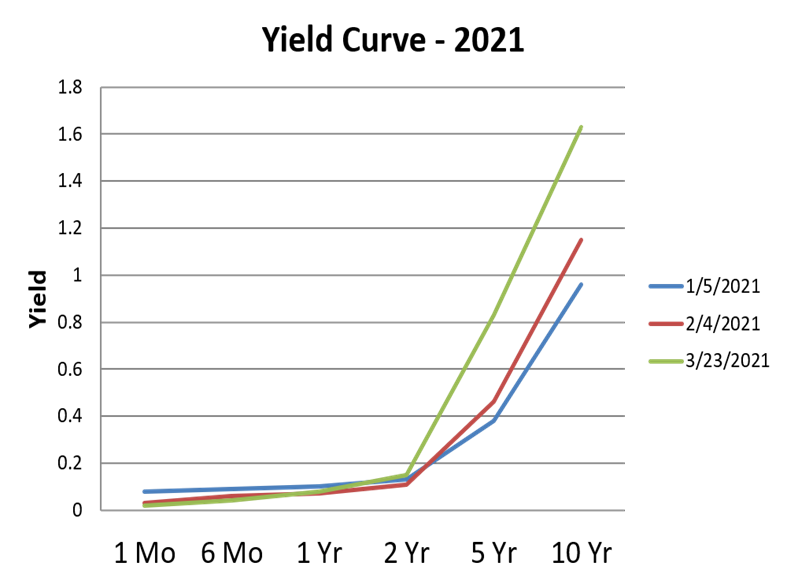

The long-term bond yields had risen in early 2021 on signs that economy is reviving. With the increase in vaccine rollouts and another large stimulus package in 2021, optimism kept growing that economy will soon be back to normal and interest rates will start rising eventually. However, at that time most of the analyst did not expect the FED to increase short-term interest rate targets anytime soon. Though, the market had priced in a potential interest rate increase in near future based on rising inflation, reducing unemployment rate & improving economy.

Now, fast forward to today, the center of the news has been the risk of inversion of the yield curve. Historically an inversion of the yield curve has been an indicator of impending recession though this is not always accurate, and we have seen false positives in the past. Markets tend to pay more attention to the spread between short term 2-year Treasury note and long term 10-year Treasury. The yield curve slightly inverted and for a short period of time in the last week of March 2022 i.e., 2-year (2.44%) notes were yielding higher than 10- year (2.391%). But others such as the Fed, pay more attention to difference between 3-month (0.533%) and 10-year (2.391%) – where there is no inversion. The National Bureau of Economic Research (NBER)— defines a recession as “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.”

We are in a unique and unprecedented situation today due to higher inflation, supply chain disruptions, no sign of end to the Russia and Ukraine crisis and the relentless Covid-19 surge in cases across globe. U.S. Inflation is at records high with March 2022 data coming up at 8.5% (CPI). To combat higher inflation, the Fed raised Fed Fund rates for the first time since the pandemic by 25 basis points and has signaled seven rate hikes in 2022. Market is pricing in 50 basis point hike in next May meeting and the future markets are pricing in Fed Fund rate to be around 2.5% by year end. The Fed is aiming at reducing liquidity from the financial system by tightening the monetary policy. In other words, reducing the supply of money to curb inflation. This makes money more expensive to borrow and less widely available.

Rise in Interest Rate’s typical effects are:

When Central Banks change interest rates, it has ripple effects throughout the economy.

- Lowering the interest rates makes borrowing cheaper. This encourages consumer and business spending. However, when interest rates increase, it has a reversal effect on borrowings and spending’s and reduces consumer confidence.

- Rising interest environment negatively impact companies that are highly leveraged for example “Tech companies”.

- Banks are generally profitable as they benefit from higher interest rate. The lending rate goes up (mortgage rate increases) and thus increasing profit margins.

- Inflation tends to increase as well, although the real interest rate (nominal interest rate minus inflation) could still be positive.

- Interest rates also impact bond prices. There is an inverse relation between bond prices and interest rates. Longer maturity bond prices tend to be more volatile in relation to interest rates.

- Higher interest rates have positive impact on dollar. Increase in interest rate attracts foreign investments and thus increasing the demand and value of home country’s currency.

The recession is not imminent yet, but it is time to bring back on our radar. Economic readings and data have been weaking recently, which is likely to continue for the near future and thus increasing the probabilities of a recession.

About the Author:

Komal Motwani, CFP ® is a Senior Investment Analyst, with over 10 years of experience in the field of Investments and Financial Planning. She has worked and studied in institutions across the globe, from India to Singapore and the US.

Disclosure: Komal Motwani, CFP ® is a senior investment analyst at Yanni & Associates Investment Advisors, LLC., a Pennsylvania-based registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

{kind=link}